The Nevada Mortgage Modification Program: How Chapter 13 Can Save Your Home When Nothing Else Will

If you are behind on your mortgage in Las Vegas and your lender has told you there are no modification options available, I want you to read this article carefully. There is a program in Nevada that most homeowners — and many attorneys — do not know exists. It has saved homes for clients of mine who had been told repeatedly that nothing could be done.

It is called the Mortgage Modification Program, or MMP. It runs through the United States Bankruptcy Court for the District of Nevada, and to participate, you have to be in a Chapter 13 bankruptcy.

I am Dan Riggs, the founder of Riggs Law Firm. I have spent more than fifteen years in bankruptcy practice in Nevada, including representing a bankruptcy trustee. Today I focus on helping people in the Las Vegas area use Chapter 7 and Chapter 13 to actually solve their financial problems — not just postpone them. MMP is one of the most powerful tools we have for homeowners, and it is dramatically underused.

What the Nevada Mortgage Modification Program Does

The Mortgage Modification Program is a court-supervised mediation between you and your mortgage lender. The bankruptcy court does not modify your mortgage itself — your lender does — but the court provides the structure, the deadlines, and the neutral oversight that often makes a deal possible where private modification efforts have failed.

In cases I have handled, the results have included some combination of the following:

- Arrearages forgiven or restructured into the modified loan

- Interest rates reduced

- Monthly payments brought down to an affordable level

- Loan terms extended

The single most important benefit, in my experience, is that the arrears stop hanging over my client’s head. When you are months or years behind on your mortgage, that pile of past-due payments feels like a wall you can never climb. MMP is one of the few tools that can actually take that wall down.

Every case is different, and there is no guarantee of any particular outcome — the lender ultimately has to agree. But MMP creates a real forum where the conversation can happen on a level playing field.

Why You Have to Be in Chapter 13

MMP is only available through Chapter 13. There are a few reasons that matter:

- Chapter 13 gives you an immediate stay against foreclosure when you file, which buys time for the modification process.

- Chapter 13 includes a structured plan to handle your other debts so the modification can actually succeed long-term.

- The bankruptcy court has jurisdiction to compel the lender to participate in mediation in good faith.

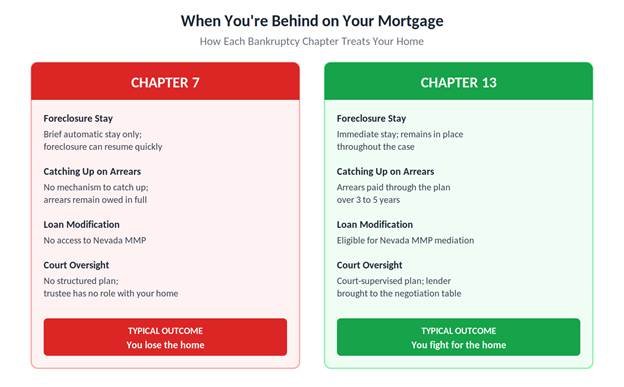

In a Chapter 7, none of that infrastructure exists. The automatic stay is short, there is no repayment plan to support a modification, and the trustee has no role in your home. If you file Chapter 7 significantly behind on your mortgage, you are typically going to lose the house. Chapter 13 is the path that lets you fight for it.

Figure 1: Chapter 7 versus Chapter 13 — what each chapter does for a homeowner behind on the mortgage.

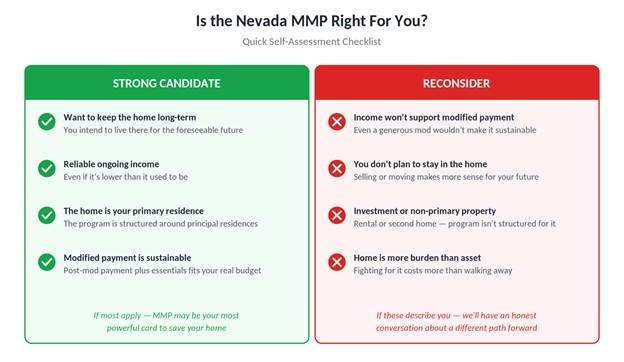

Who Is a Good Candidate for the Mortgage Modification Program

MMP is not the right tool for everyone. In my office, before I recommend a Chapter 13 with MMP, I want to see most of the following:

- You want to keep the home and intend to live in it for the foreseeable future

- You have a reliable, ongoing income — even if it is lower than it used to be

- The home is your primary residence (the program is structured around principal residences)

- Your post-modification payment, plus your other essential expenses, would actually be sustainable on your real budget

If those things are true, MMP is often the most powerful card you can play. If you are still weighing your options between Chapter 7 and Chapter 13, see our detailed guide: Chapter 7 vs Chapter 13: Which Bankruptcy Is Right for You?

Figure 2: Quick self-assessment — which side describes your situation more accurately?

When MMP Is Not the Right Answer

I will be direct with you: I have seen homeowners — and frankly, attorneys — get into Chapter 13 cases trying to save homes that cannot be saved. The math does not work. The household income cannot support the modified payment even after the modification. The case fails twelve or eighteen months in, and the homeowner has spent thousands of dollars in attorney fees and plan payments only to lose the home anyway.

That is the worst outcome in bankruptcy practice, and I will not let it happen at Riggs Law Firm. Part of my job is to look at the numbers honestly and tell you whether saving the home is realistic. If it is not, we have a different conversation — about how to walk away with dignity, protect what assets you do have, and use bankruptcy to set you up for the next chapter of your life. Sometimes the best advice I can give a client is, “this home is not the right place to plant your flag.”

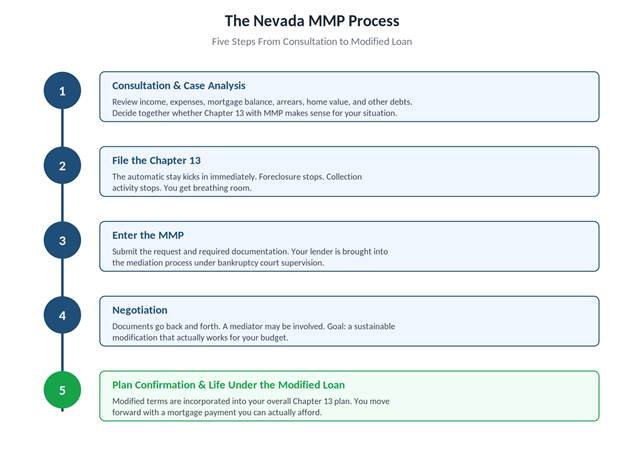

What the Nevada Mortgage Modification Program Process Looks Like

In broad strokes, here is what to expect:

Figure 3: The five-step path from initial consultation to a confirmed plan with a modified mortgage.

Throughout the process, you continue to live in your home, and you have an attorney handling the lender on your behalf.

The Trustee’s Eye on Your Case

Here is where my background matters. I represented a bankruptcy trustee for more than fifteen years and conducted thousands of 341 Meetings of Creditors. I know what trustees look for. I know what judges expect. I know how lenders position themselves in mediation and what kinds of proposals tend to land.

That experience shapes how I prepare a Chapter 13 with MMP from day one. Your budget needs to be defensible. Your asset disclosures need to be complete and accurate. Your proposed plan needs to make sense to a trustee who is going to review it carefully. Cases that are sloppy on these points do not get the same traction in mediation.

If You Are Behind, Do Not Wait

The hardest part of mortgage cases is timing. Once a foreclosure sale is set, the options narrow quickly. Once a sale has happened, most options are gone entirely. If you are behind on your mortgage and have been told by your lender that there are no modification options — or if you have simply been getting nowhere — call before things get worse, not after.

Talk to Riggs Law Firm

If you are weighing Chapter 7 against Chapter 13 — or wondering whether bankruptcy is the right move at all — the most valuable thing you can do is sit down with an attorney who will give you a frank, honest assessment of your options. Our debt solutions page outlines all of the tools available to Las Vegas homeowners facing financial hardship.

At Riggs Law Firm, I bring more than fifteen years of bankruptcy experience to every case, including extensive work representing a bankruptcy trustee. That background means I see your case from both sides of the table before we ever file.

Contact Riggs Law Firm or call 702-605-5070 to schedule a consultation. We will lay out your options, answer your questions, and help you decide what fits your life.

Disclaimer: This article is for general informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship with Riggs Law Firm. Every bankruptcy case is fact-specific. For advice about your particular situation, please contact a licensed Nevada bankruptcy attorney. Riggs Law Firm is a debt relief agency. We help people file for bankruptcy relief under the U.S. Bankruptcy Code.