Here is something I hear in my office almost every week: “I would file Chapter 7, but my income is too high. Somebody told me I do not qualify.” What most people do not realize is that the Chapter 7 means test exceptions built into the Bankruptcy Code can change that answer entirely.

Sometimes that is true. Often it is not. The means test — the income calculation that determines whether you can file a Chapter 7 — is governed by federal bankruptcy law and has exceptions that are written right into the Bankruptcy Code but rarely make it into general advice. If you have been told you do not qualify, this article is for you.

I am Dan Riggs, the founder of Riggs Law Firm. I have practiced bankruptcy law in Nevada for more than fifteen years, including extensive work representing a Chapter 13 bankruptcy trustee. I have seen both sides of how the means test gets applied, and I want to walk you through what most people miss.

The General Rule

Generally speaking, if your household income over the six months before filing is above the median income for the state of Nevada for your household size, you cannot file a Chapter 7 — or at least, not without going through a more complex analysis that often disqualifies you.

Median income figures change periodically and depend on household size, so I will not put specific dollar amounts in this article. The takeaway is simple: above median income usually pushes you into Chapter 13 territory.

Usually. Not always.

Means Test Exceptions #1: Debts Mostly Incurred From a Failed Business

This is the most overlooked exception in the entire means test, and it has saved Chapter 7 filings for clients of mine who had been told by other lawyers that they were over income.

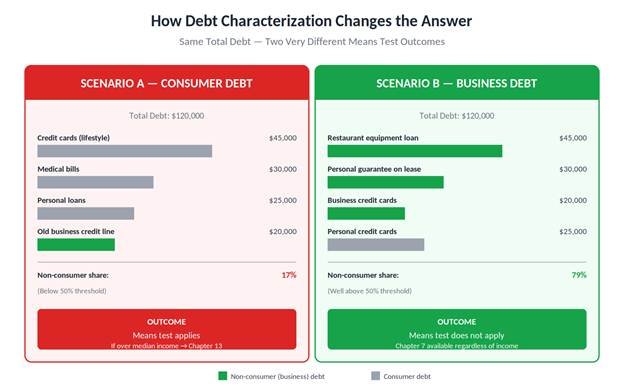

The Bankruptcy Code includes a category called “non-consumer debt” — debt that was incurred for a business purpose rather than for personal, family, or household use. If more than half of your total debt falls in that category, the means test does not apply to you at all. You can file Chapter 7 even if your income is well above the Nevada median.

This matters enormously in real life. Think about the people who come out of a failed business in our area:

- A restaurant owner who personally guaranteed equipment loans, lease obligations, and supplier accounts

- A contractor who took on credit lines and equipment financing to keep a job moving

- A small retailer who used personal credit cards to float inventory and payroll during a slow stretch

- A real estate investor whose rental portfolio collapsed and left personal guarantees behind

If more than half the total debt is tied to the business, the means test analysis changes completely. These are exactly the clients who often have enough current income to look “over median” — but who genuinely need a clean break, not a five-year repayment plan.

Two things to understand. First, the analysis is dollar-weighted, not count-weighted. Five credit cards in your name for groceries do not outweigh one big business loan if the business loan is larger. Second, the characterization of each debt matters and is not always obvious. A credit card used partly for business and partly personally requires careful analysis. This is the kind of case that benefits from an attorney who knows what they are looking at.

Figure 1: Same total debt amount, but the composition of the debt determines whether the means test applies.

Means Test Exceptions #2: Qualifying Disabled Veterans

The second major exception is for certain disabled veterans. If you are a disabled veteran whose indebtedness was incurred primarily during active duty or while performing homeland defense activities, you may be exempt from the means test even if your current income is above the Nevada median.

The specifics — the disability rating required, what counts as active duty or homeland defense, and how the debts must be tied to that service — are written into the Bankruptcy Code. If you have served and are now carrying significant debt from that period, this is not a long-shot argument. It is a recognized statutory exemption from the means test.

If you served, please mention it at our consultation. Do not assume it is irrelevant. The means test treats your situation differently than a civilian’s, and you deserve to know that going in.

Why the Means Test Exceptions Matter in Practice

These exceptions are not loopholes. They are deliberate choices by Congress about who the means test is and is not designed for. Congress did not want failed business owners or disabled veterans funneled into mandatory five-year repayment plans on the same terms as someone who ran up consumer credit cards on lifestyle spending.

But because most general advice about bankruptcy focuses on the W-2 employee with consumer debt, these exceptions get glossed over. I have had clients come to me after being told flatly by other attorneys that Chapter 7 was off the table — and I have filed successful Chapter 7 cases for them because someone actually ran the right analysis.

If you are still working out whether Chapter 7 or Chapter 13 makes more sense for your situation overall, our guide Chapter 7 vs Chapter 13: Which Bankruptcy Is Right for You? walks through the key differences in detail.

Even Without Means Test Exceptions, You Have Options

If neither exception applies and your income is currently above median, there are still moves worth considering:

- Timing. The means test looks at the six months before filing. If your income has recently dropped, waiting a month or two can change the calculation entirely.

- Job changes. If your hours have been cut, or you have lost a second job, your six-month average will eventually catch up to your new reality.

- Chapter 13 as a strategic choice. If Chapter 7 is genuinely out of reach right now, Chapter 13 still does powerful work — and a well-structured Chapter 13 plan in Nevada can be far more favorable than people expect.

- Conversion. If you file Chapter 13 now because of your income, and then later lose a job or have hours cut, your case can sometimes be converted to a Chapter 7. I have had many clients start in Chapter 13 and convert when their income dropped.

A Word About the Trustee’s Perspective

Because I represented a Chapter 7 trustee for more than fifteen years, I want to be direct about one thing: claiming an exception you do not actually qualify for is not a strategy. Trustees scrutinize means test exceptions carefully. The U.S. Trustee’s office reviews these filings. Misclassifying debts to dodge the means test is the kind of thing that draws unwanted attention to your entire case.

The right approach is the honest one: gather the documentation, characterize each debt correctly, and let the law work the way Congress designed it. When the exception fits, it fits — and there is nothing the trustee can do about that. When it does not fit, we plan a different strategy. You can explore your full range of debt solutions with us at a free consultation.

If You Have Been Told You Cannot File

If you have been told you do not qualify for Chapter 7 because of your income, understanding the means test exceptions built into the code is worth reviewing before you accept that conclusion:

- Was more than half of your total debt incurred for a business purpose?

- Are you a disabled veteran with debts from active duty or homeland defense activities?

- Has your income recently dropped, or is it about to?

- Did the person who told you no actually run the means test, or did they look at your gross pay and stop there?

If the answer to any of those is yes — or even maybe — it is worth a real conversation. Contact Riggs Law Firm to schedule a free consultation and get a real answer.

Talk to Riggs Law Firm

If you are weighing Chapter 7 against Chapter 13 — or wondering whether bankruptcy is the right move at all — the most valuable thing you can do is sit down with an attorney who will give you a frank, honest assessment of your options. Our debt solutions page outlines every tool available to Las Vegas residents facing financial hardship.

At Riggs Law Firm, I bring more than fifteen years of bankruptcy experience to every case, including extensive work representing a Chapter 13 bankruptcy trustee. That background means I see your case from both sides of the table before we ever file.

Contact Riggs Law Firm or call 702-605-5070 to schedule a consultation. We will lay out your options, answer your questions, and help you decide what fits your life.

Disclaimer: This article is for general informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship with Riggs Law Firm. Every bankruptcy case is fact-specific. For advice about your particular situation, please contact a licensed Nevada bankruptcy attorney. Riggs Law Firm is a debt relief agency. We help people file for bankruptcy relief under the U.S. Bankruptcy Code.