What Happens to Your Credit After Bankruptcy?

One of the biggest fears people have about filing bankruptcy is the impact on their credit score. You’ve probably heard that bankruptcy will “ruin your credit for 7-10 years” or that “you’ll never get a loan again.”

At Riggs Law Firm, we hear these concerns every day from our Las Vegas clients. Here’s the truth: while bankruptcy does affect your credit, the impact is often less severe than you think, and recovery is faster than most people realize. Even better, bankruptcy often improves your credit faster than continuing to struggle with debt you can’t pay. (For a step-by-step look at the process, see our guide to credit repair after bankruptcy.)

The Initial Impact on Your Credit Score

Let’s be direct: filing bankruptcy will lower your credit score, at least initially. The bankruptcy filing itself is a significant negative mark on your credit report.

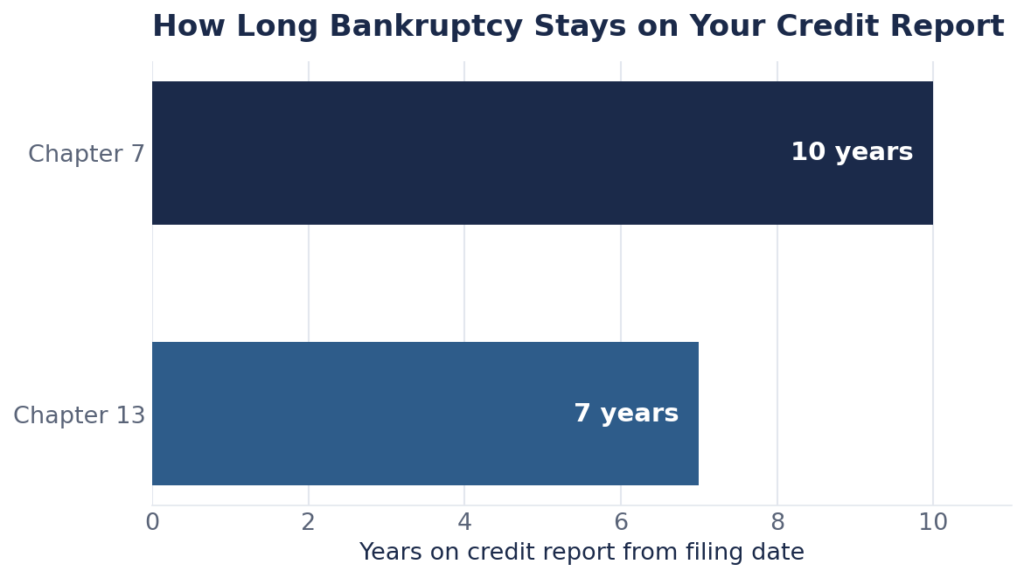

How Long Bankruptcy Stays on Your Credit Report

- Chapter 7: Remains for 10 years from the filing date

- Chapter 13: Remains for 7 years from the filing date

However, the presence of bankruptcy on your report and its actual impact on your ability to get credit are two different things. Here’s what most people don’t understand: the negative impact diminishes significantly over time, especially if you’re rebuilding your credit responsibly. (Learn more about how long bankruptcy stays on your credit report.)

Why Your Credit Might Already Be Damaged

If you’re considering bankruptcy, your credit score is probably already suffering. Here are factors that may already be hurting your credit:

- Late Payments: Every payment that’s 30, 60, or 90+ days late damages your credit score. These late payments stay on your report for 7 years.

- High Credit Utilization: Maxed-out credit cards or high balances relative to your credit limits severely impact your score.

- Collections Accounts: Once an account goes to collections, it’s a major negative mark.

- Charge-Offs: When a creditor writes off your debt as uncollectible, it devastates your score.

- Judgments and Liens: Court judgments and tax liens are extremely damaging.

- Inquiries from Desperate Credit Seeking: Multiple credit applications in a short time hurt your score.

If your credit report already shows several of these issues, you may be surprised to find that bankruptcy doesn’t lower your score as much as you’d expect—because your credit is already significantly damaged.

The Bankruptcy Paradox: Sometimes Your Credit Improves Faster

Here’s something most people don’t realize: filing bankruptcy can actually help your credit score recover faster than continuing to struggle with unpayable debt.

Why Bankruptcy Can Help Your Credit

When you file bankruptcy, you eliminate debt rather than continuing to miss payments and accumulate late payment marks. Your credit report goes from showing:

Before Bankruptcy:

- Multiple accounts with late payments every month

- High credit utilization (maxed cards)

- Collection accounts

- Possibly judgments or garnishments

- An ever-worsening pattern

After Bankruptcy:

- One bankruptcy filing notation

- Debts showing $0 balance

- No new late payments

- No collection activity

- A clean slate to rebuild from

The bankruptcy is one negative mark versus dozens of ongoing negative marks. Over time, demonstrating responsible credit use after bankruptcy rebuilds your score faster than years of struggling with unpayable debt.

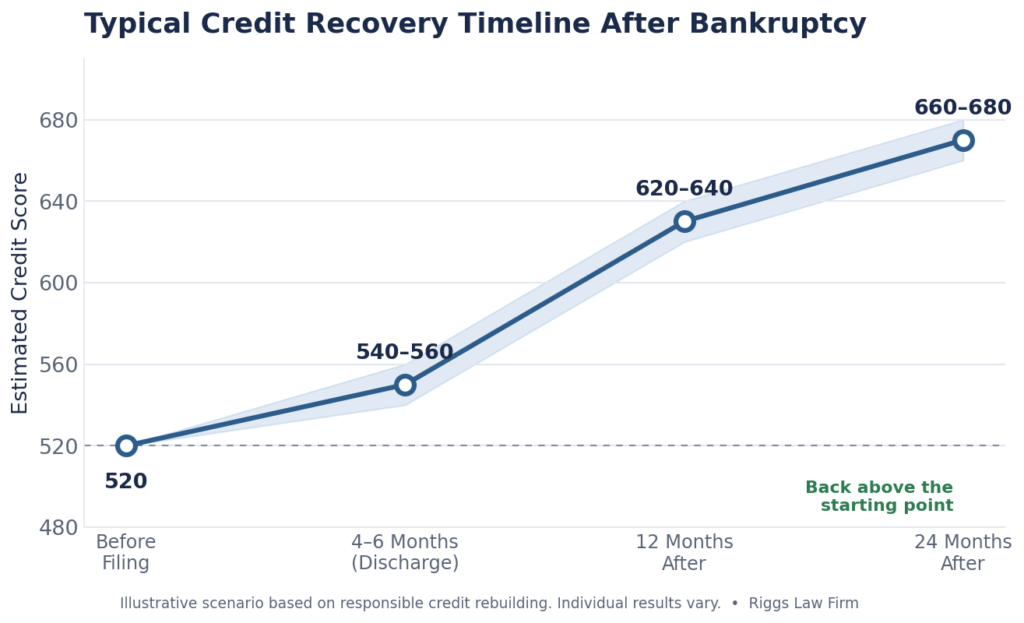

Real Client Example: Credit Recovery Timeline

Let’s look at a typical scenario we see at Riggs Law Firm:

Before Bankruptcy:

- Credit score: 520

- $45,000 in credit card debt across 8 cards, all maxed out

- 6 months of late payments on most accounts

- 2 accounts in collections

- 1 wage garnishment

Immediately After Chapter 7 Discharge (4-6 months later):

- Credit score: 540-560 (slight increase or minimal decrease)

- All discharged debts showing $0 balance

- No ongoing late payments

- Garnishment stopped

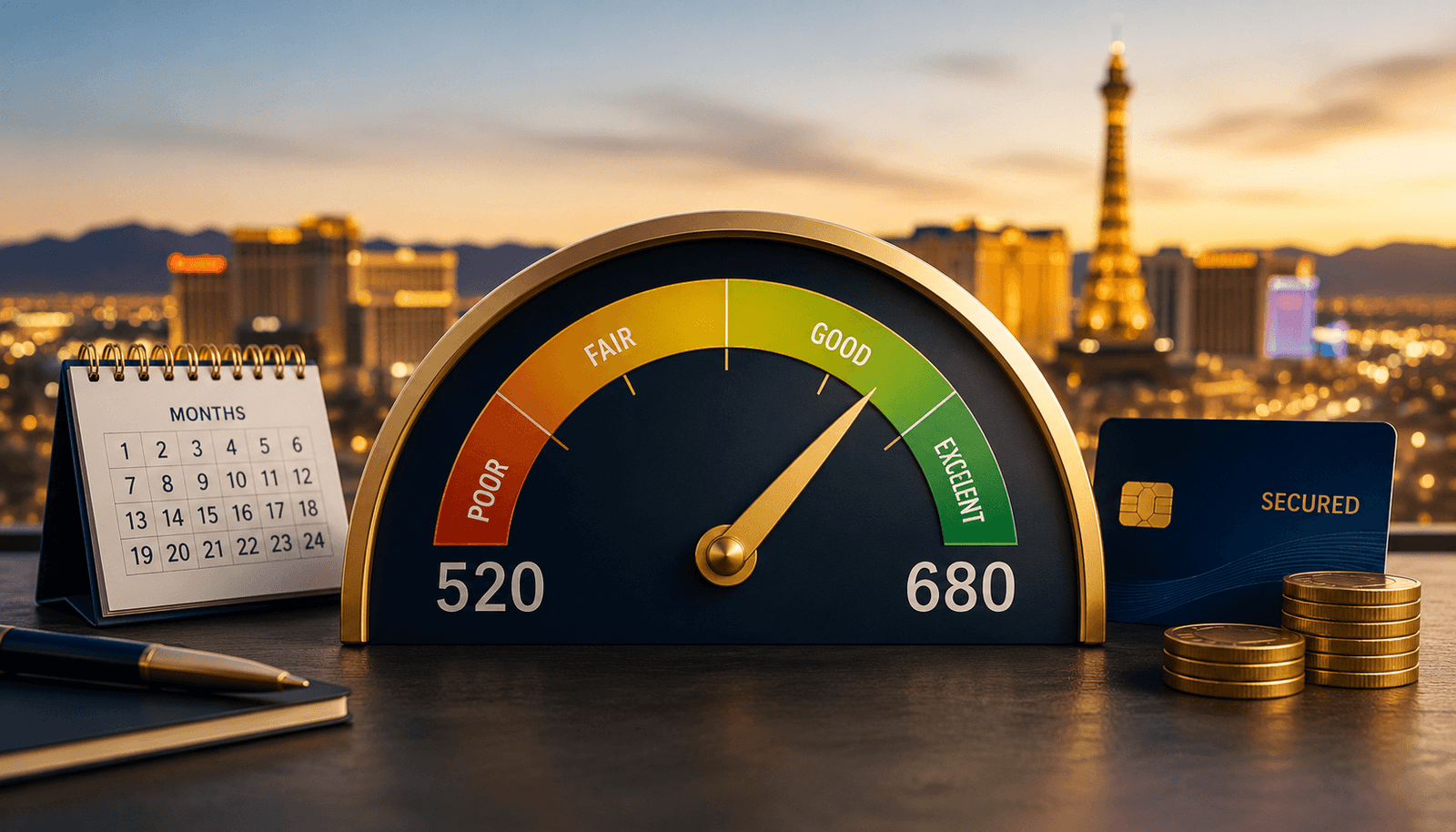

12 Months After Bankruptcy:

- Credit score: 620-640

- Secured credit card with perfect payment history

- Auto loan with regular payments

- Positive payment history rebuilding

24 Months After Bankruptcy:

- Credit score: 660-680

- Multiple credit accounts in good standing

- Possibly pre-approved for conventional mortgage

- Credit score higher than before filing

This timeline assumes responsible credit rebuilding. Some clients recover even faster, especially if they had good credit before their financial crisis.

The Three Phases of Credit Recovery

Phase 1: Immediate Post-Bankruptcy (0-6 Months)

Your score may initially drop or stay about the same. This is when the bankruptcy first appears on your report. However, you’ll notice immediate relief:

- No more collection calls

- No more late payment marks accumulating

- No more maxed-out credit cards dragging down your score

- No more judgments or garnishments

Phase 2: Early Rebuilding (6-18 Months)

This is when you’ll see the most improvement. As you establish new positive payment history:

- Secured credit cards with perfect payments boost your score

- Auto loans (if needed) add positive payment history

- The weight of the bankruptcy filing starts to diminish

- Your credit score typically improves 100+ points

Phase 3: Solid Recovery (18 Months – 4 Years)

Your credit continues to strengthen:

- You may qualify for conventional mortgages (FHA loans available even sooner)

- Credit card offers increase

- Better interest rates become available

- The bankruptcy becomes less and less important to your overall credit profile

How to Rebuild Your Credit After Bankruptcy

At Riggs Law Firm, we don’t just help you file bankruptcy—we guide you through credit rebuilding. Here are the strategies that work:

1. Get a Secured Credit Card Immediately

A secured credit card requires a deposit that becomes your credit limit. It’s the fastest way to start rebuilding.

Best practices:

- Start with a $300-500 secured card within 30-60 days of discharge

- Use it for small, regular purchases (gas, groceries)

- Pay the FULL balance every month—never carry a balance

- After 6-12 months, many issuers convert it to an unsecured card and return your deposit

Recommended cards for post-bankruptcy:

- Discover it® Secured Card

- Capital One Platinum Secured

- OpenSky® Secured Visa®

2. Become an Authorized User

If you have a family member with good credit who trusts you, ask to be added as an authorized user on their credit card. Their positive payment history will appear on your credit report.

Important: Make sure the account holder has:

- Long history with the card

- Perfect payment history

- Low credit utilization

- A card issuer that reports authorized users to credit bureaus

3. Get a Credit Builder Loan

These small loans are designed specifically for credit rebuilding. The bank holds the loan amount in an account while you make monthly payments. After you’ve paid it off, you get the money.

Credit unions often offer these for $500-1,000 with reasonable terms. The perfect payment history helps rebuild your credit.

4. Keep Credit Utilization Below 30% (Preferably Below 10%)

Once you have credit again, never use more than 30% of your available credit. Keeping it under 10% is even better.

Example: If you have a secured card with a $500 limit, keep your balance below $50-150 at all times.

5. Pay Everything On Time, Every Time

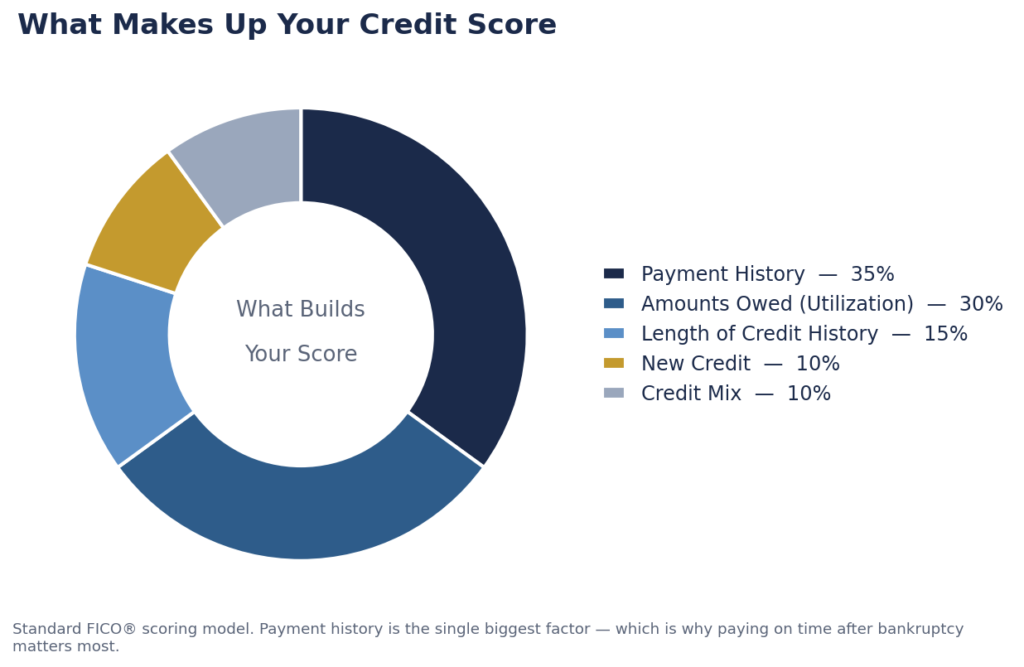

Payment history is the single biggest factor in your credit score (35%). Even one late payment can significantly damage your rebuilding efforts.

Set up automatic payments if necessary. A single $25 monthly payment on time is more valuable for your credit than large purchases you pay off in full.

6. Monitor Your Credit Reports Regularly

You’re entitled to free credit reports from all three bureaus (Equifax, Experian, TransUnion) once per year at AnnualCreditReport.com.

Check for:

- Accounts that should have been discharged but still show balances

- Incorrect late payment marks after your filing date

- Discharged debts being sold to new collectors (this violates the discharge order)

If you find errors, dispute them immediately. We can help you with this process.

7. Diversify Your Credit (Eventually)

In time, having different types of credit (credit cards, auto loan, personal loan) helps your score. But don’t rush this—start with one secured card and build from there.

Common Credit Rebuilding Mistakes to Avoid

- Applying for Too Much Credit Too Soon: Multiple credit applications hurt your score. Be selective and strategic.

- Carrying Balances to “Build Credit”: This is a myth. You don’t need to pay interest to build credit. Pay your full balance monthly.

- Falling for Credit Repair Scams: No company can remove accurate information from your credit report, including a legitimately filed bankruptcy. Save your money.

- Ignoring Your Credit: Some people are so traumatized by their financial crisis that they avoid looking at their credit. Monitor it regularly and stay engaged in the rebuilding process.

- Taking on Debt You Can’t Afford: The point of bankruptcy is a fresh start. Don’t rush into car loans or other debt just to rebuild credit faster. Only take on debt you can easily afford.

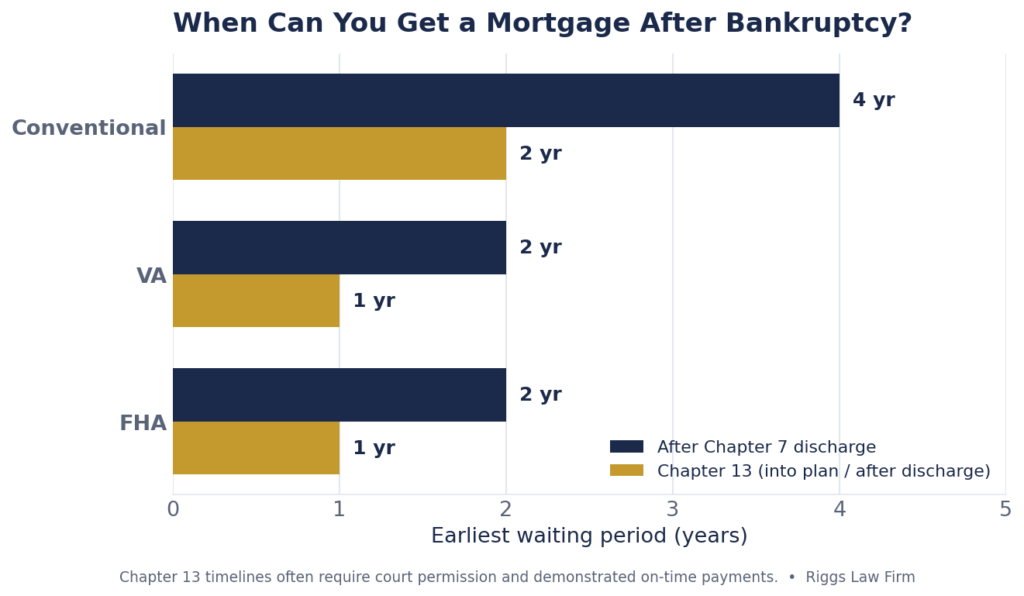

When Can You Get a Mortgage After Bankruptcy?

This is one of the most common questions we hear. The good news: you don’t have to wait 7-10 years. If keeping your home is your main concern, learn how a Chapter 13 plan can stop foreclosure and save your home.

FHA Loans:

- Available 2 years after Chapter 7 discharge

- Available 1 year into a Chapter 13 plan (with court permission)

- Require credit scores as low as 580 (though 620+ is better)

Conventional Loans:

- Available 4 years after Chapter 7 discharge

- Available 2 years after Chapter 13 discharge

- Typically require credit scores of 620+

VA Loans (for veterans):

- Available 2 years after Chapter 7 discharge

- Often available 1 year into a Chapter 13 plan

- More flexible requirements

The key is demonstrating responsible credit use during the waiting period. Clients who follow our credit rebuilding advice often qualify for mortgages at the earliest possible dates.

When Can You Get a Car Loan After Bankruptcy?

Many of our clients are surprised to learn they can get auto loans very soon after bankruptcy—sometimes even before discharge.

Special Financing for Post-Bankruptcy:

- Some lenders specialize in post-bankruptcy auto loans

- Available sometimes within months of filing

- Interest rates are higher initially but can be refinanced later

Best Practices for Post-Bankruptcy Auto Loans:

- Wait a few months after discharge if possible

- Save for a down payment (10-20%)

- Don’t overextend—buy a reliable used car, not your dream car

- Make every payment on time to rebuild credit

- Refinance after 12-18 months of perfect payments to get a better rate

The Emotional Side of Credit Rebuilding

Beyond the numbers, credit rebuilding is an emotional journey. Many of our Las Vegas clients feel shame or embarrassment about bankruptcy at first. Here’s what we want you to know:

Bankruptcy is a financial tool, not a moral failure. Millions of Americans file bankruptcy every year for reasons beyond their control: medical emergencies, job loss, divorce, economic downturns.

Your credit score doesn’t define you. It’s a number that reflects your current financial situation, and numbers can change.

You’re not starting from zero. You’re starting from a position of freedom—free from overwhelming debt, free from creditor harassment, free to rebuild strategically.

The best revenge is success. The most satisfying thing for our clients is when, two years later, they’re buying a home or a car with credit they’ve rebuilt themselves.

How Riggs Law Firm Helps With Credit Rebuilding

At Riggs Law Firm, our service doesn’t end when your bankruptcy is discharged. We help you rebuild your credit and financial future:

- Post-Bankruptcy Credit Counseling: We provide guidance on exactly how to rebuild your credit step-by-step.

- Credit Monitoring Support: We help you check your credit reports for errors and dispute inaccuracies.

- Ongoing Advice: Even after your case is closed, we’re available to answer questions about credit rebuilding.

- Referrals: We can connect you with credit unions and lenders who work with post-bankruptcy clients.

- Educational Resources: We provide materials and guidance to help you make smart financial decisions going forward.

Not sure which chapter is right for you? Explore our overview of Las Vegas debt solutions, or compare Chapter 7 and Chapter 13 bankruptcy. Wondering about fees? See how much bankruptcy costs in Nevada.

Your Fresh Start Begins Now

Bankruptcy gives you a fresh start financially, but it’s up to you to make the most of it. The clients who rebuild their credit fastest are those who:

- Start rebuilding immediately after discharge

- Make every payment on time

- Keep credit utilization low

- Stay patient and consistent

- Avoid the mistakes that led to bankruptcy in the first place

Yes, bankruptcy affects your credit. But it’s not the end of your financial life—it’s the beginning of a better one. With the right strategy and commitment, you can rebuild your credit faster than you think and achieve financial goals that seemed impossible when you were drowning in debt.

Ready to start your fresh start? Contact Riggs Law Firm today for a free consultation. Call 702-605-5070 or schedule online. We’ll help you eliminate your debt and guide you through rebuilding your credit for a stronger financial future. We proudly serve Las Vegas, Henderson, North Las Vegas, and Summerlin.

Your credit score doesn’t have to define you. Let’s rebuild it together.

This article provides general information about credit rebuilding after bankruptcy and does not constitute legal or financial advice. Individual results vary based on personal circumstances and credit rebuilding efforts. Contact Riggs Law Firm for personalized guidance.