Most people think of Chapter 13 bankruptcy as a tool for wiping out credit cards and medical bills. It absolutely is that. But the debts that are quietly destroying most of the people I meet are not the credit cards — they are the debts that bankruptcy supposedly cannot discharge. IRS balances. Back child support. Alimony arrears. Student loans.

Here is what almost no one tells you: even though Chapter 7 cannot discharge those debts, Chapter 13 still has powerful things to say about them. In many cases, Chapter 13 is the single most effective tool available for dealing with this category of debt.

I am Dan Riggs, the founder of Riggs Law Firm in the Las Vegas area. After more than fifteen years in bankruptcy practice — including representing a Chapter 7 trustee — I want to walk you through how Chapter 13 actually handles these debts and why it can mean the difference between a fresh start and just trading one problem for another.

The Core Problem With Chapter 7 and Non-Dischargeable Debt

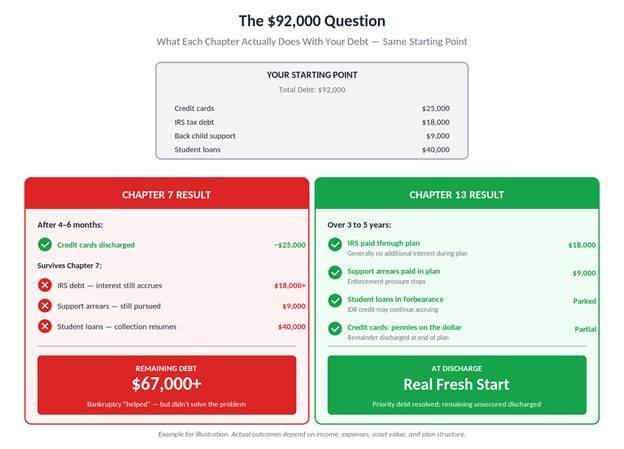

Picture this scenario. You owe $25,000 in credit cards, $18,000 to the IRS, $9,000 in back child support, and $40,000 in student loans. You file a Chapter 7. Four months later, the credit cards are gone.

And you are still on the hook for $67,000 in non-dischargeable debt, with interest and penalties continuing to grow on the IRS balance, the support enforcement agency still pursuing you for the arrears, and your loan servicer cycling through collection efforts on the student loans. The Chapter 7 helped. It did not solve the problem.

Figure 1: The same $92,000 starting debt — what each chapter actually leaves you with.

This is where Chapter 13 changes the picture. Inside a Chapter 13 plan, those non-dischargeable debts are not just sitting on the sidelines. They are being handled — actively, methodically, and on terms much more favorable than what you can get outside bankruptcy.

IRS and State Tax Debt

Tax debt is one of the most powerful reasons to consider Chapter 13. Inside a Chapter 13 plan, priority tax debt can be paid down over three to five years — and crucially, it is generally paid without additional interest accruing during the plan. The penalties that would normally pile up while you are trying to catch up just stop. The plan is your protected runway.

Some older tax debt may actually be dischargeable in Chapter 13 (and Chapter 7) if it meets specific timing and filing requirements. The rules are technical. But the broad point is this: a Chapter 13 plan gives the IRS an organized, court-supervised way to be paid, and gives you protection from levies, garnishments, and the spiral of penalties while you do it.

Compare that to the alternative. Outside of bankruptcy, IRS installment agreements continue to accrue interest. Offer in Compromise programs work for some taxpayers but not others. Wage garnishments and bank levies can resume at any time. Chapter 13 puts all of that on pause and gives you a fixed plan.

Child Support and Alimony Arrears

Domestic support obligations are some of the most aggressively collected debts in the system, and for good reason — children and former spouses depend on them. Bankruptcy does not discharge support obligations, and it should not.

But Chapter 13 still helps in a specific, important way. The arrears — the back amount you owe — can be paid through your Chapter 13 plan over the life of the case. The wage withholding, the threats to your professional license, the inability to renew your driver’s license in some cases, the constant pressure from enforcement — those things settle down when there is a confirmed plan paying the arrears in a structured way.

Two important caveats. First, you still have to pay your current ongoing support during the Chapter 13 — that does not go through the plan. Second, the arrears must be paid in full by the end of the plan. So this works when the arrears are large but bounded; it does not work to discharge support.

For many of my clients, that is exactly the help they need. The current support they can handle. It is the mountain of arrears that has been suffocating them, and the Chapter 13 gives them a way to climb it without losing everything else along the way.

Student Loans — Including the Income-Driven Repayment Wrinkle

Student loans are notoriously difficult to discharge in bankruptcy. There are paths to discharge in extreme hardship cases, and the law in this area has been shifting, but for most filers, you should plan on coming out of bankruptcy still owing your student loans.

Here is what Chapter 13 does for student loan borrowers that most people have no idea about.

During your Chapter 13, your student loans generally go into forbearance. You are not required to make payments on them while you are in the plan. The Chapter 13 plan payment is what your budget can sustain; the student loan is parked.

Now here is the part that almost nobody knows. If you are enrolled in an income-driven repayment program — IDR — you generally continue to receive credit toward forgiveness for the months you are in your Chapter 13 bankruptcy, even though you are not making payments. Programs and rules can change, and the details depend on your specific program and loan type, so this is a conversation to have carefully. But for many borrowers, the practical effect is that you keep advancing toward forgiveness while in bankruptcy, while paying nothing on the loan and using that breathing room to address everything else.

For a borrower with significant student debt who is on the path to IDR forgiveness, this is one of the most quietly valuable features of Chapter 13.

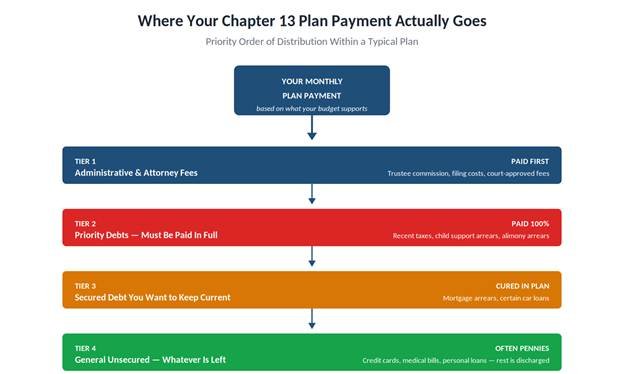

Why Chapter 13 Plans Often Pay Less Than You Think

Clients sometimes come in afraid that a Chapter 13 will require them to pay everything they owe. That is almost never the case.

In a typical Chapter 13, you pay 100% of your priority debt (taxes, support arrears) and your secured debt that you want to keep current (like your mortgage arrears and certain car loans). You pay your unsecured creditors — credit cards, medical bills, personal loans — only a percentage of what is owed, based on what your budget can support and what the law requires. Many of my clients end up paying their unsecured creditors pennies on the dollar over the life of the plan.

Figure 2: How your monthly plan payment flows through priority levels — non-dischargeable debt gets paid first.

The non-dischargeable debt is what makes Chapter 13 such a strategic tool. You are using your monthly plan payment to actually demolish the debts that would have survived a Chapter 7, while wiping out a meaningful portion of the unsecured debt at the same time. At the end of the plan, you owe what was paid in full (the priority debt) and you walk away from what remains of the unsecured debt. That is a real fresh start — not just the elimination of credit cards.

The Strategic Re-Routing of Asset Value

Here is a tactic that comes from my trustee background. Sometimes a client has an asset they cannot fully exempt — equity in a second vehicle, for example, or a tax refund, or an inheritance. In a Chapter 7, the trustee would liquidate that asset and distribute the proceeds to unsecured creditors. The client loses the asset, and the credit card companies get a check.

In a Chapter 13, that same value gets paid in to the plan over three to five years — and it can be applied to priority debts like back taxes, support arrears, or other non-dischargeable obligations. Instead of losing the asset and watching the value go to your credit card companies, you keep the asset and the same dollars wipe out a debt that would otherwise have followed you out of Chapter 7.

That is the kind of redirect that experienced bankruptcy lawyers think about. It is exactly the analysis that separates a bankruptcy filed strategically from a bankruptcy filed reflexively.

Who Should Be Thinking About This

If you owe meaningful amounts in any of the following categories, Chapter 13 deserves a serious look — even if Chapter 7 is technically available to you:

- IRS or state income tax debt of more than a few thousand dollars

- Back child support or alimony arrears

- Student loans, especially if you are pursuing IDR forgiveness

- Other priority debts like certain government fines or judgments

A Chapter 7 alone might leave those debts sitting on you in full. A well-structured Chapter 13 might handle them in a way that no other tool — bankruptcy or otherwise — can match.

Talk to Riggs Law Firm

If you are weighing Chapter 7 against Chapter 13 — or wondering whether bankruptcy is the right move at all — the most valuable thing you can do is sit down with an attorney who will give you a frank, honest assessment of your options.

At Riggs Law Firm, I bring more than fifteen years of bankruptcy experience to every case, including extensive work representing a Chapter 7 bankruptcy trustee. That background means I see your case from both sides of the table before we ever file.

Call Riggs Law Firm at 702-605-5070 to schedule a consultation. We will lay out your options, answer your questions, and help you decide what fits your life.Disclaimer: This article is for general informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship with Riggs Law Firm. Every bankruptcy case is fact-specific. For advice about your particular situation, please contact a licensed Nevada bankruptcy attorney. Riggs Law Firm is a debt relief agency. We help people file for bankruptcy relief under the U.S. Bankruptcy Code