The saddest cases I see in my office are not the people who file bankruptcy. They are the people who spent down everything the law would have protected — trying to avoid filing bankruptcy — and then had to file anyway — without first calling a bankruptcy attorney.

I am Dan Riggs, the founder of Riggs Law Firm. I have spent more than fifteen years in bankruptcy practice in Nevada, including representing a Chapter 7 bankruptcy trustee. If there is one piece of advice I would give to anyone in serious financial distress, it is this: before you make any major financial move to try to pay down debt, call a bankruptcy attorney for a consultation. Not to file. To talk.

A consultation costs nothing or very little. The mistakes I am about to describe can cost tens or hundreds of thousands of dollars and years of recovery time.

Protected Money Is Real

United States and Nevada law protects certain assets from creditors — even if you eventually file bankruptcy. Among the most important categories:

- Most retirement accounts (401(k)s, IRAs within limits, pensions)

- A significant amount of equity in your homestead under Nevada’s homestead exemption

- A meaningful amount of equity in one vehicle

- Tools of your trade up to a statutory limit

- Certain types of insurance benefits and proceeds

- Public benefits, Social Security, disability

Specific limits and rules change and depend on your facts. The takeaway is bigger than any single number: there are categories of money the law has decided to leave alone, because Congress and the Nevada Legislature have decided you need them more than your creditors do.

Figure 1: The fundamental mismatch — voluntarily moving money from the left side to the right side is exactly what the law was designed to prevent.

When you voluntarily spend those protected assets to pay unsecured creditors, you are doing exactly what the law was designed to prevent.

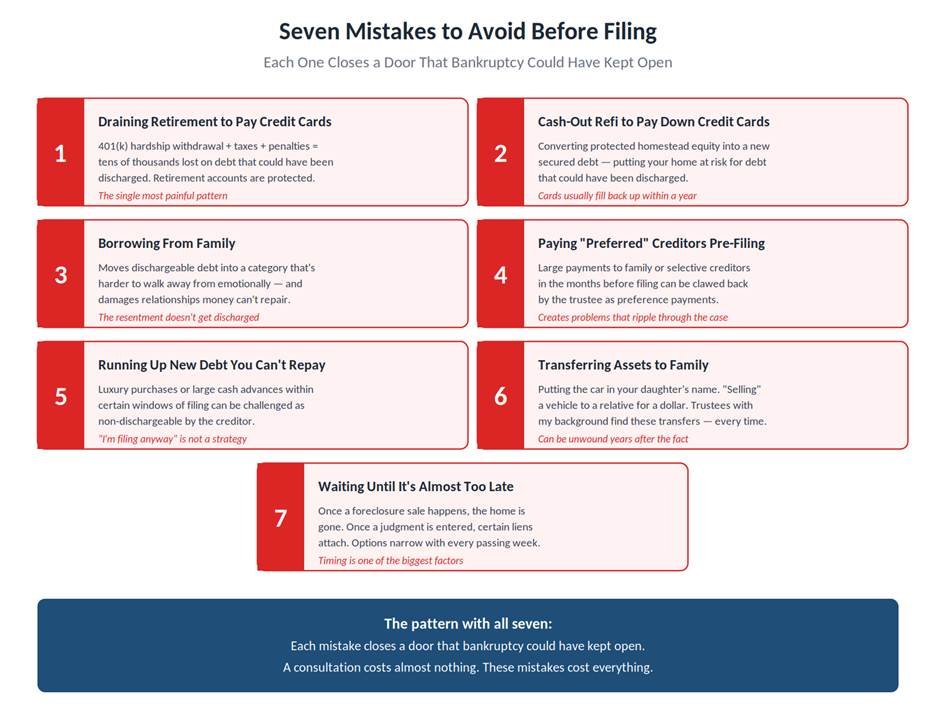

The Mistakes That Hurt the Most

Figure 2: The seven most common — and most costly — mistakes people make in the months before filing.

Each of those deserves a deeper look. Here is the detail behind each.

1. Draining Retirement Accounts to Pay Credit Cards

This is the single most painful pattern I see. A client takes a hardship distribution from a 401(k), or empties an IRA, to pay down credit card debt. They pay taxes on the withdrawal. They pay early withdrawal penalties. They reduce their retirement savings — sometimes by tens of thousands of dollars — and the credit cards still are not paid off because the original problem (income not covering ongoing expenses) was never solved.

Six months later, they file bankruptcy anyway. The retirement money is gone. The credit card debt that the bankruptcy would have wiped out is mostly still there. And on top of everything, they owe taxes on the withdrawal.

If they had called me before the withdrawal, we likely could have protected the retirement account and discharged the credit cards. That money — sometimes a lifetime of savings — would still be there. This is the heartbreak of the practice.

2. Pulling Equity Out of Your Home to Pay Down Unsecured Debt

Nevada’s homestead exemption is generous. For most homeowners, a substantial amount of equity in your primary residence is protected from creditors. When you take a home equity loan or a cash-out refinance to pay down credit cards, you are converting protected equity into a new secured debt against your home. You have just put your house at risk to pay debts that, in many cases, you could have discharged.

Worse, the underlying cash flow problem usually is not solved. Now you have a smaller home equity cushion and a larger monthly payment, and the credit cards often start filling back up within a year or two.

3. Borrowing From Family

This one is not just a financial mistake — it is a relational one. I have watched debt destroy more family relationships than just about anything else.

If you borrow $20,000 from your parents or your sibling to pay down credit card debt, two things happen. First, you have moved dischargeable debt into a category that is harder to walk away from emotionally. Second, you have put a relationship that matters more than money into the middle of the worst part of your financial life. When the underlying problem is not solved, the resentment that builds up cannot be discharged in any court.

Bankruptcy is designed for exactly this. It lets you handle the debt without dragging the people you love into it.

4. Paying “Preferred” Creditors Right Before Filing

This one is more technical, and it is one of the reasons it pays to talk to a bankruptcy lawyer before you make major payments. Bankruptcy law has rules about “preference” payments — money you paid to certain creditors in the period before filing — and those rules sometimes let the trustee claw the money back from the creditor.

In particular, large payments to family members in the year before filing can be unwound by a trustee after the case is filed. So if you sell your motorcycle to your brother for less than it is worth, or pay off the loan from your mother three months before filing, you may be setting up a problem that ripples through your bankruptcy.

There are also rules about preferential payments to ordinary creditors in the 90 days before filing that can become an issue in certain cases. None of this means do not pay your bills — it means do not make unusual, large, or selective payments in the months before bankruptcy without legal advice.

5. Running Up New Debt You Cannot Repay

Charges made shortly before filing — particularly large purchases or cash advances — can be challenged by creditors as non-dischargeable. There are presumptive rules about luxury goods and cash advances within certain windows of the filing date. Loading up credit cards because “I am going to file anyway” is a real way to keep some of that debt from being discharged.

6. Transferring Assets to Family

Putting the car in your daughter’s name. “Selling” the boat to your brother-in-law for a dollar. Quitclaiming the rental property to your spouse. These transfers can be unwound by the trustee, sometimes years after the fact. They can also raise questions about your honesty in the case as a whole. Almost no transfer made in the year or two before a bankruptcy filing is invisible to a trustee with my background.

7. Waiting Until After a Lawsuit Is Filed or a Garnishment Begins

Bankruptcy can stop most lawsuits and most garnishments. But the longer you wait, the more options narrow. Once a foreclosure sale has happened, the home is generally gone. Once a wage garnishment is taking real money out of every paycheck, the financial situation gets worse every two weeks until you file. Once a judgment is entered, certain liens may attach to property in ways that complicate the case.

Timing matters. If you are being sued, do not wait until the morning of the hearing to think about bankruptcy.

The Conversation That Changes the Trajectory

What I want — what I really want — is for people in financial trouble to talk to a bankruptcy attorney before they make any large, irreversible decision. Not because I want to file every case. Sometimes I tell people that bankruptcy is not the right tool right now. Sometimes I refer them to a credit counselor, or a tax attorney, or a divorce lawyer, or a non-profit, or simply tell them what their best non-bankruptcy options look like.

But that conversation cannot happen after you have emptied your retirement account or borrowed against your home. By then, the most valuable cards have already been thrown away.

Signs You Should Call a Bankruptcy Attorney Now, Not Later

If any of the following describe your situation, this is the call to make today:

- You are thinking about borrowing from a 401(k), IRA, or other retirement account to pay debt

- You are considering a home equity loan or cash-out refinance to pay credit cards

- You are thinking about borrowing significant money from family

- Debt has put you in a position where you cannot reliably pay rent, food, utilities, or medication

- You have been sued by a creditor, or a lawsuit is imminent

- Your wages are about to be garnished, or already are

- Your home is in foreclosure or a sale date has been set

- Tax debt is growing faster than you can pay it down

- You are paying minimums on credit cards and watching the balances grow instead of shrink

An Honest Assessment, Not a Sales Pitch

When you call Riggs Law Firm, I will give you an honest assessment of your situation. If bankruptcy is the right tool — Chapter 7 or Chapter 13 — we will discuss exactly how it would work for you. If there is a better option outside of bankruptcy, I will tell you. If your situation is one where waiting and reassessing in a few months makes sense, I will tell you that too.

My goal is not to file your case. My goal is to help you make a decision you will look back on in five years and be grateful for. Often that means filing. Sometimes it does not. Either way, the value of the conversation is in the honest analysis — and that conversation is worth far more than the call itself.

Talk to Riggs Law Firm

If you are weighing Chapter 7 against Chapter 13 — or wondering whether bankruptcy is the right move at all — the most valuable thing you can do is sit down with an attorney who will give you a frank, honest assessment of your options.

At Riggs Law Firm, I bring more than fifteen years of bankruptcy experience to every case, including extensive work representing a Chapter 7 bankruptcy trustee. That background means I see your case from both sides of the table before we ever file.

Call Riggs Law Firm at 702-605-5070 to schedule a consultation. We will lay out your options, answer your questions, and help you decide what fits your life.

Disclaimer: This article is for general informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship with Riggs Law Firm. Every bankruptcy case is fact-specific. For advice about your particular situation, please contact a licensed Nevada bankruptcy attorney. Riggs Law Firm is a debt relief agency. We help people file for bankruptcy relief under the U.S. Bankruptcy Code.